README

Riskfolio-Lib

Portfolio Optimization in Python, Easy for Everyone.

Riskfolio-Lib helps users perform portfolio optimization and quantitative strategic asset allocation directly within Python.

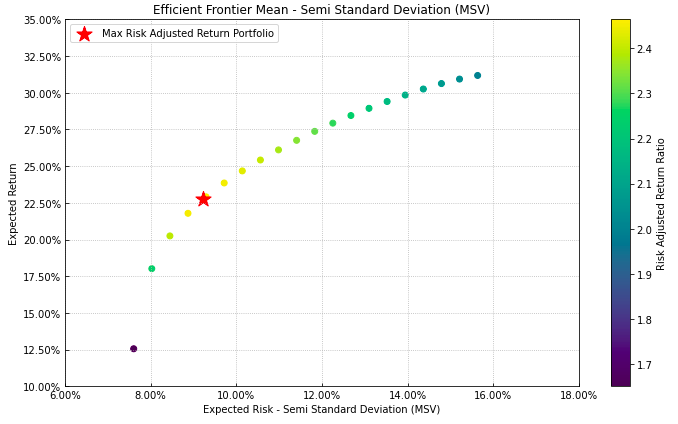

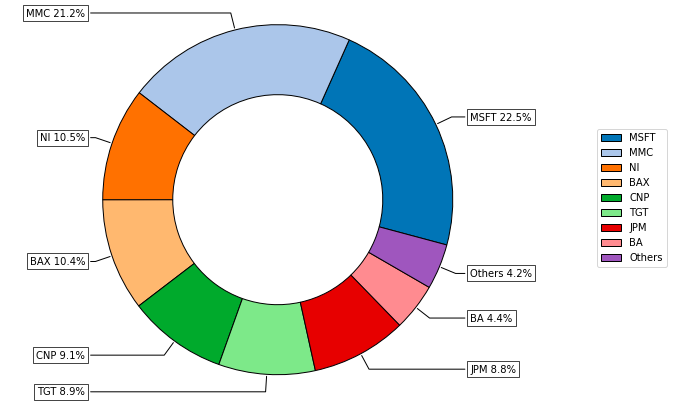

This Python library offers various tools for constructing optimal investment portfolios using models like Mean-Semivariance, CVaR, and drawdown. It calculates efficient frontiers and executes strategic asset allocation, with typical outputs including visualizations such as the shown MSV Frontier and Pie Chart. Users interact with the library by importing it and calling functions to define assets, set constraints, and apply different optimization methods.

Riskfolio-Lib helps users perform portfolio optimization and quantitative strategic asset allocation directly within Python.

Quantitative analysts, financial researchers, and investors seeking programmatic control over portfolio management and risk assessment will find this useful.

Portfolio Optimization in Python, Easy for Everyone.