Reversal 3.3

Reversal 3.3 Live Paper Test

- Latest checkpoint (ET):

2026-04-25 02:55:07 EDT

- Equity:

$13,955.50 | Realized: $4,045.50 | Unrealized: $-90.00 | Open positions: 1

- Today closed trades:

0

- Current slot:

share_ext_0255

- Universe:

qqq_plus_leverage_etfs

- Chart windows:

Overall / 1D / 1W / 1M (default open panel: Overall)

Current Open Positions

ticker asset_type execution_mode instrument units cash_spent current_position_value current_price unrealized_pnl unrealized_return_pct business_days_held

TXN option option TXN260618C00280000 4 5790.0 5700.0 14.25 -90.0 -1.55 0

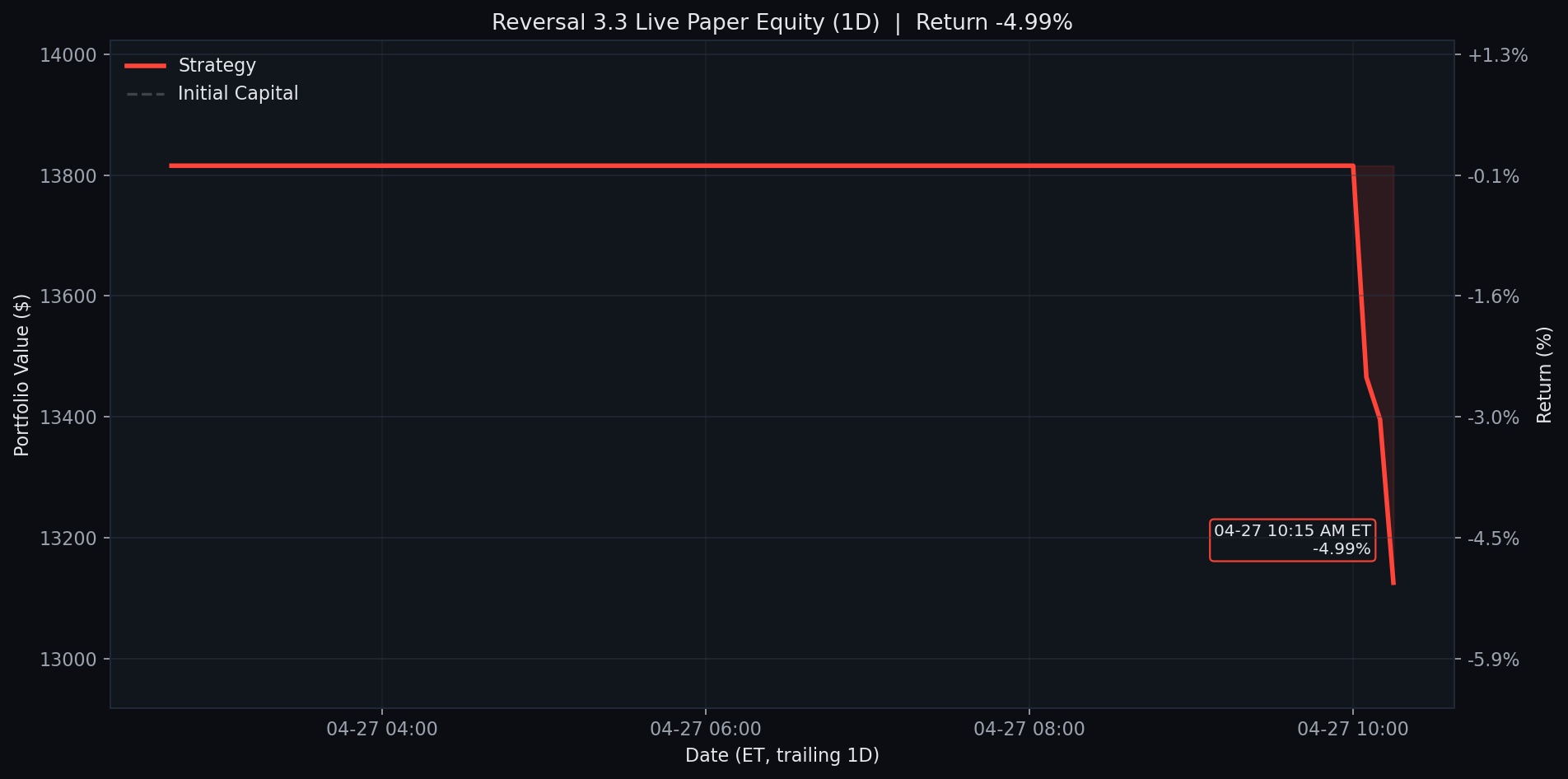

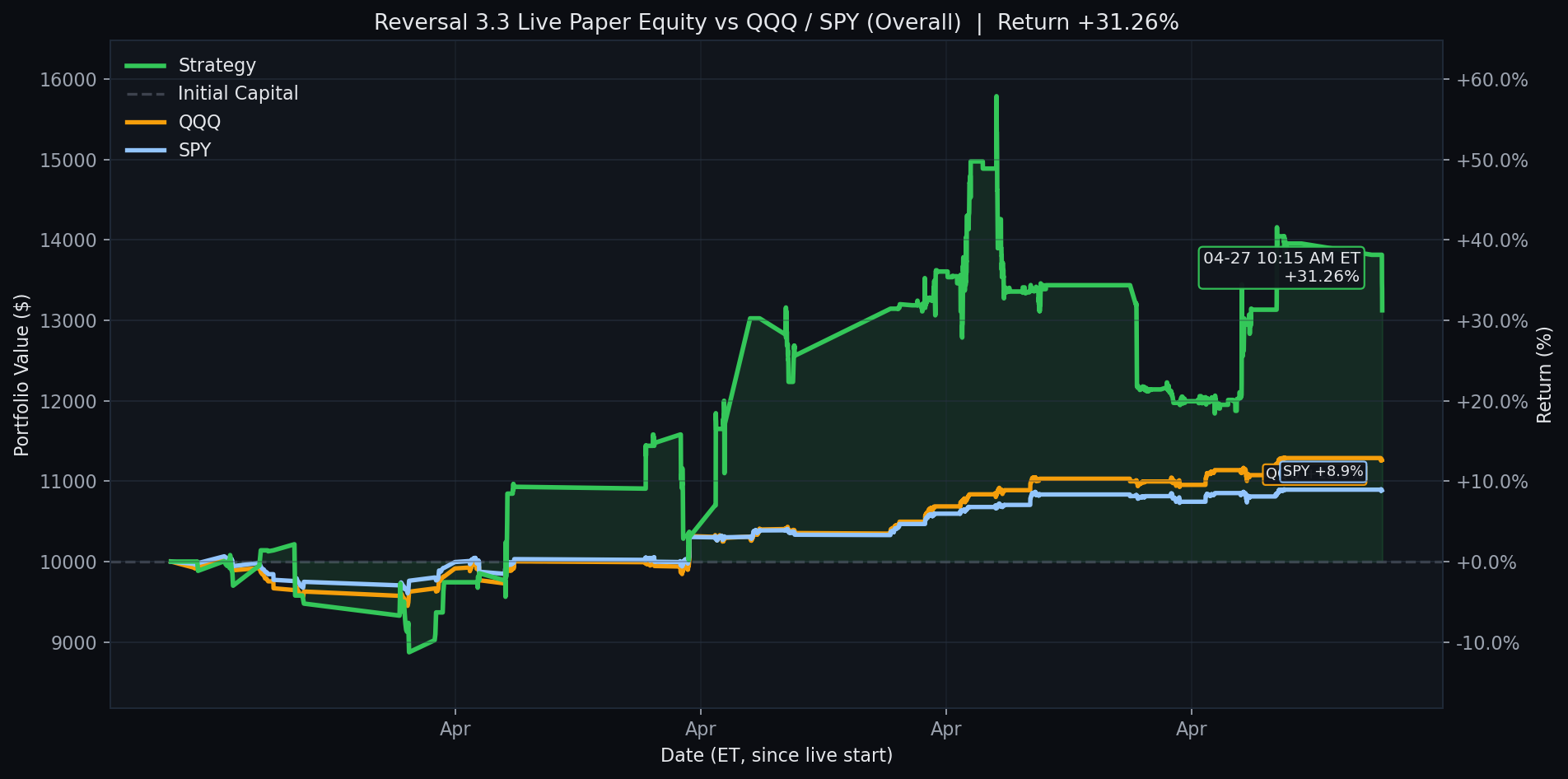

Overall

1D