README

Modeling High-Frequency Limit Order Book Dynamics Using Machine Learning

-

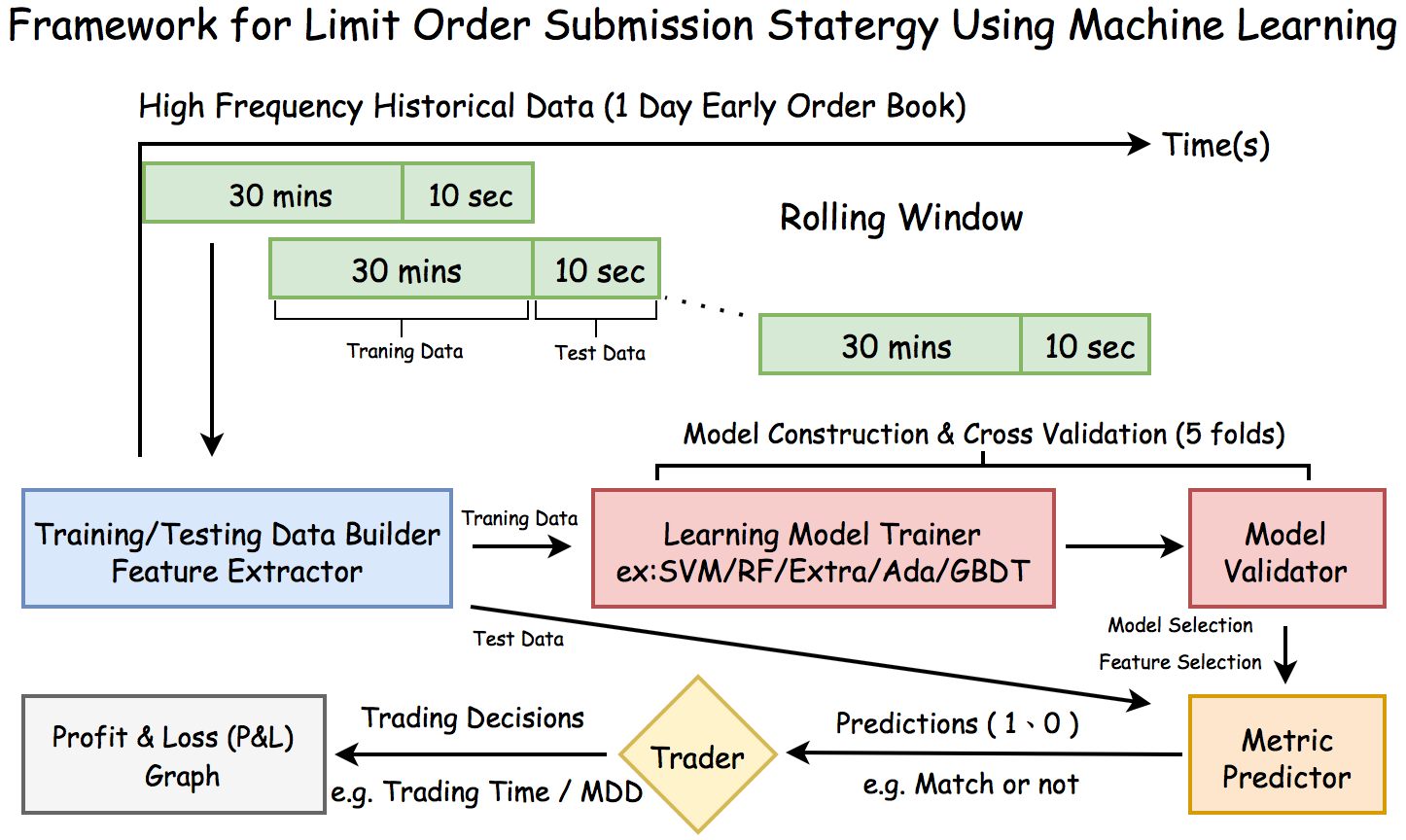

Framework to capture the dynamics of high-frequency limit order books.

Overview

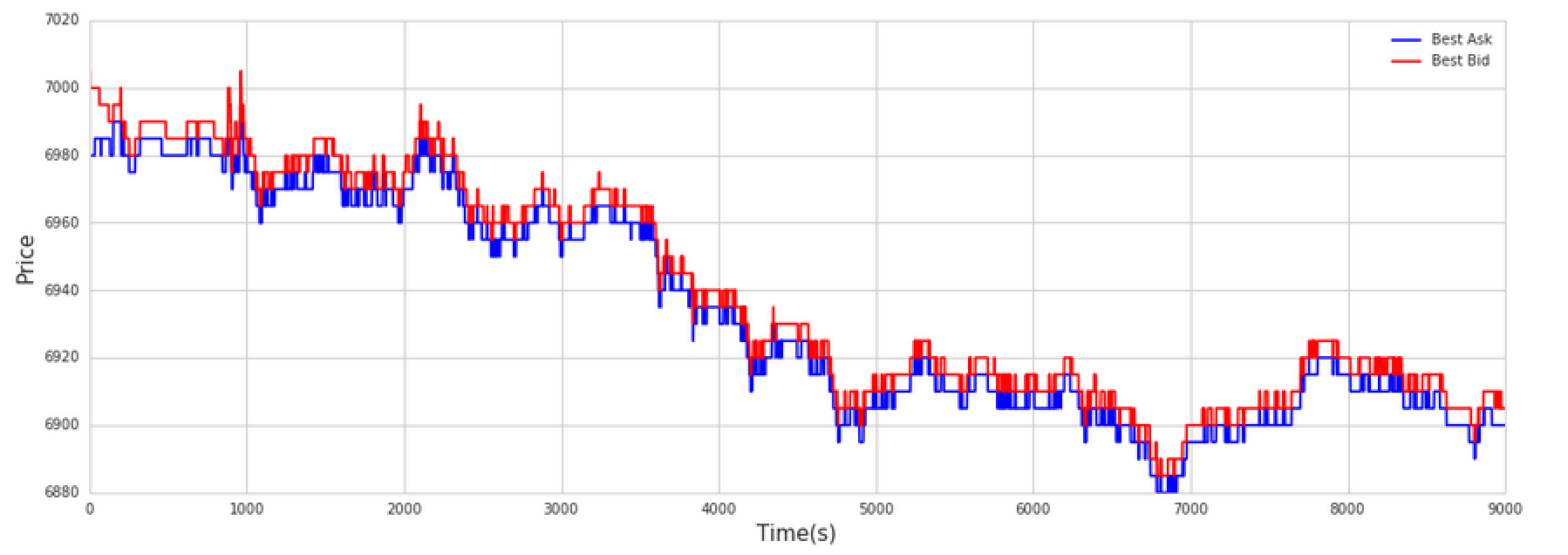

In this project I used machine learning methods to capture the high-frequency limit order book dynamics and simple trading strategy to get the P&L outcomes.

-

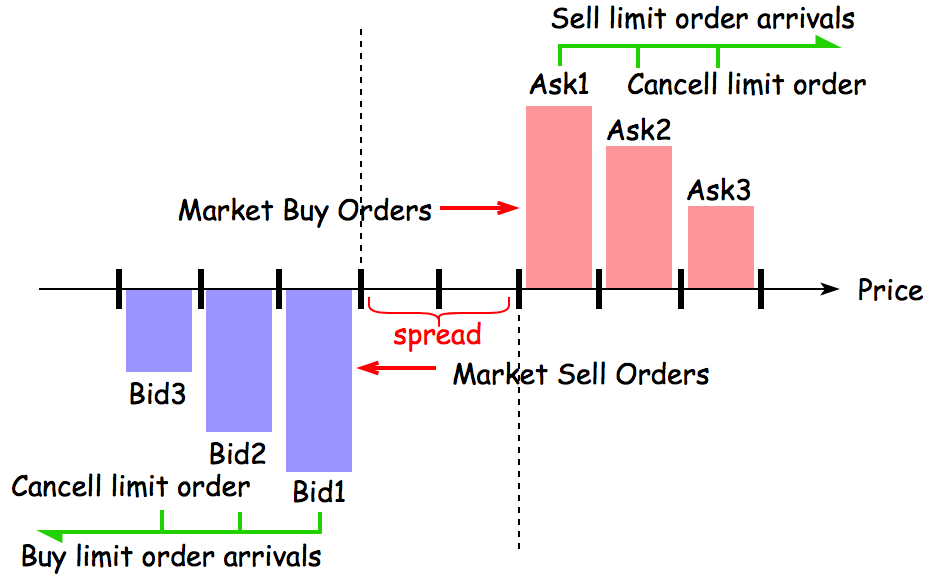

Feature Extractor

-

Rise Ratio

-

Depth Ratio

[Note] : [Feature_Selection] (Feature_Selection)

-

-

Learning Model Trainer

- RandomForestClassifier

- ExtraTreesClassifier

- AdaBoostClassifier

- GradientBoostingClassifier

- SVM